RESEARCH AND ANALYSIS

MACRO REPORT DEEP DIVE

MAY 23, 2024

One of the major themes for 1H24 is the reset in expectations away from a swift succession in interest rate cuts and towards sustained “higher-for-longer”. Unsurprisingly, the housing market continues to be the most acutely impacted and the data has softened as mortgage rates rose since January. Taking a step back, underlying demand for housing appears stable with the starts/permits pipeline above the 2019 average, but affordability will likely remain a headwind in the 2nd half of 2024.

Latest

May 31, 2024

Macro Report

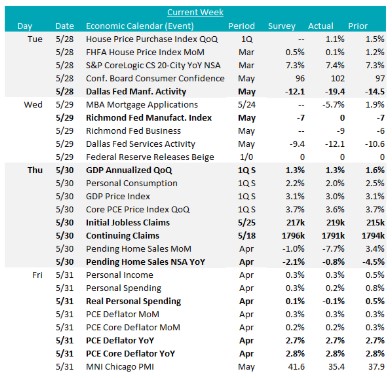

This week’s data showed mixed results from Fed manufacturing data, further softness on the housing side, and a better-than-expected inflation print.

May 30, 2024

Fundamental Report

Elevated imports and domestic production continue to be the most important story for the U.S. steel market. Until the surplus is worked through, it is hard to see a strong bullish case for prices.

May 29, 2024

Macro Flash Report

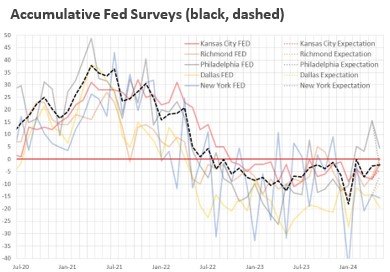

May’s Fed Manufacturing surveys improved slightly but remain in an overall contractionary position. Forward looking expectations largely remain optimistic, however, slightly less than in April. The ongoing recovery in the manufacturing sector continues to be sluggish as industrial sectors of the U.S. economy continue adjusting to a higher for longer interest rate environment.

May 24, 2024

Macro Report

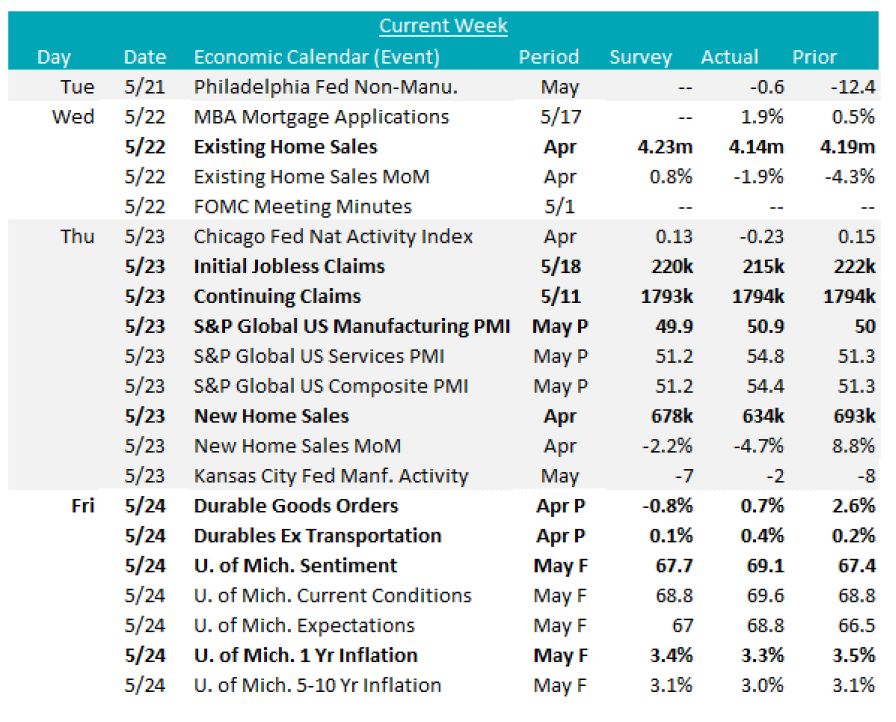

This week’s data showed stability in the manufacturing sector, but further disappointed with housing data. Overall economic activity continues to be encouraging and consumers expectations remain buoyant, but volatile.

May 23, 2024

Fundamental Report

Import arrivals trend higher, while domestic production is at the higher level of its recent range. Domestic spot prices search for a bottom as we continue converging with the global price.

May 21, 2024

Fundamental Flash Report

Domestic production increased for the 3rd week in a row, now up to 1,728k st/pw. Overall, while production has increased since the end of 4Q23 and beginning of 1Q24, we only briefly touched the historical average of 1,744k in early April. This level of production compared historical terms suggests that demand has been somewhat muted, given the fact that spot prices have been under pressure all year.

More Reports

Show More Reports